India's Economic Slowdown : Part 2

A series of policy missteps have contributed to the slowdown

I ended part 1 by discussing how the combined impact of the botched implementation of GST and demonetisation hurt the Indian economy. The policy missteps didn’t end there.

In 2019, the government attempted to address the issues plaguing the economy, but it once again took the wrong route. It announced a corporate tax cut that lowered the base rate for existing companies from 30% to 22% and for new manufacturing companies (incorporated after October 1, 2019) from 25% to 15%.

The idea was that this tax break would incentivise companies to make new investments, thereby boosting private investment in the economy. However, that private investment never materialized. Large corporations may have saved up to Rs 1 lakh crore annually as a result of the tax cut.

Instead, the tax burden on individual taxpayers increased through both direct and indirect taxes, while private investment failed to receive the expected boost. The recent move to reduce income taxes for those earning up to Rs 12 lakh per year appears to be a tacit acknowledgment that the corporate tax cut did not work.

Lack of a COVID response

Then, two years later, when COVID-19 struck, India was still not on a path to recovery. In the two quarters immediately preceding the pandemic—Q2 and Q3—the Indian economy grew at only 5.1% and 4.3%, respectively.

The government’s response to the pandemic (or the lack of one) did little to help. At a time when governments around the globe were injecting cash into their economies to support individuals and businesses, India’s approach leaned heavily on credit-based schemes and indirect measures.

While Japan and the USA introduced fiscal stimulus packages amounting to 54% and 27% of GDP, respectively, India’s fiscal stimulus was less than 5% of GDP.

The situation was further aggravated by poor governance and a lack of planning. Prime Minister Narendra Modi announced an abrupt nationwide lockdown on March 24, 2020, with just four hours’ notice, as if to catch the virus off guard.

A study found that over 44 million migrant workers were forced to return to their villages, often walking hundreds of kilometres in scorching heat. Many died during these journeys due to accidents, exhaustion, and starvation. According to data compiled by Thejesh G.N., Kanika Sharma, and Aman, 991 people died by the end of July 2020.

Adding to this mismanagement was the fact that the government was not focused on the most critical problems. For example, during the pandemic it introduced the hugely controversial farm laws. Without delving into the merits of the laws, the timing was clearly off: instead of focusing on immediate economic recovery, the government pushed through structural reforms in the midst of a crisis, sparking mass protests by farmers. In the end, the laws had to be repealed, and the promised reforms were not achieved.

At a time when the Indian economy resembled a patient in the ICU, the government did very little to keep it alive. The economy survived—and eventually bounced back—not because of government interventions but despite them.

In many respects, the post-pandemic rebound was largely statistical—a result of the low base effect.

In fact, after part 1 of my article, Professor Ashoka Mody very helpfully pointed out to me another factor behind the “high” growth rates observed in recent data. Mody has found that India’s statistical office is considering selective data to calculate India’s GDP. So, real growth rates could be even lower. For example, as low as 4.5% instead of the recorded 7.8% in Q1 of 2023-24.

Post-pandemic, Modi announced that India’s goal is to become a developed nation by 2047, yet he provided no clear roadmap for achieving this ambition. The recently released Economic Survey of 2024-25 states that India must grow at least 8% annually for a decade to reach that goal and emphasises that developing the manufacturing sector is “essential.”

Lessons from South Korea and China

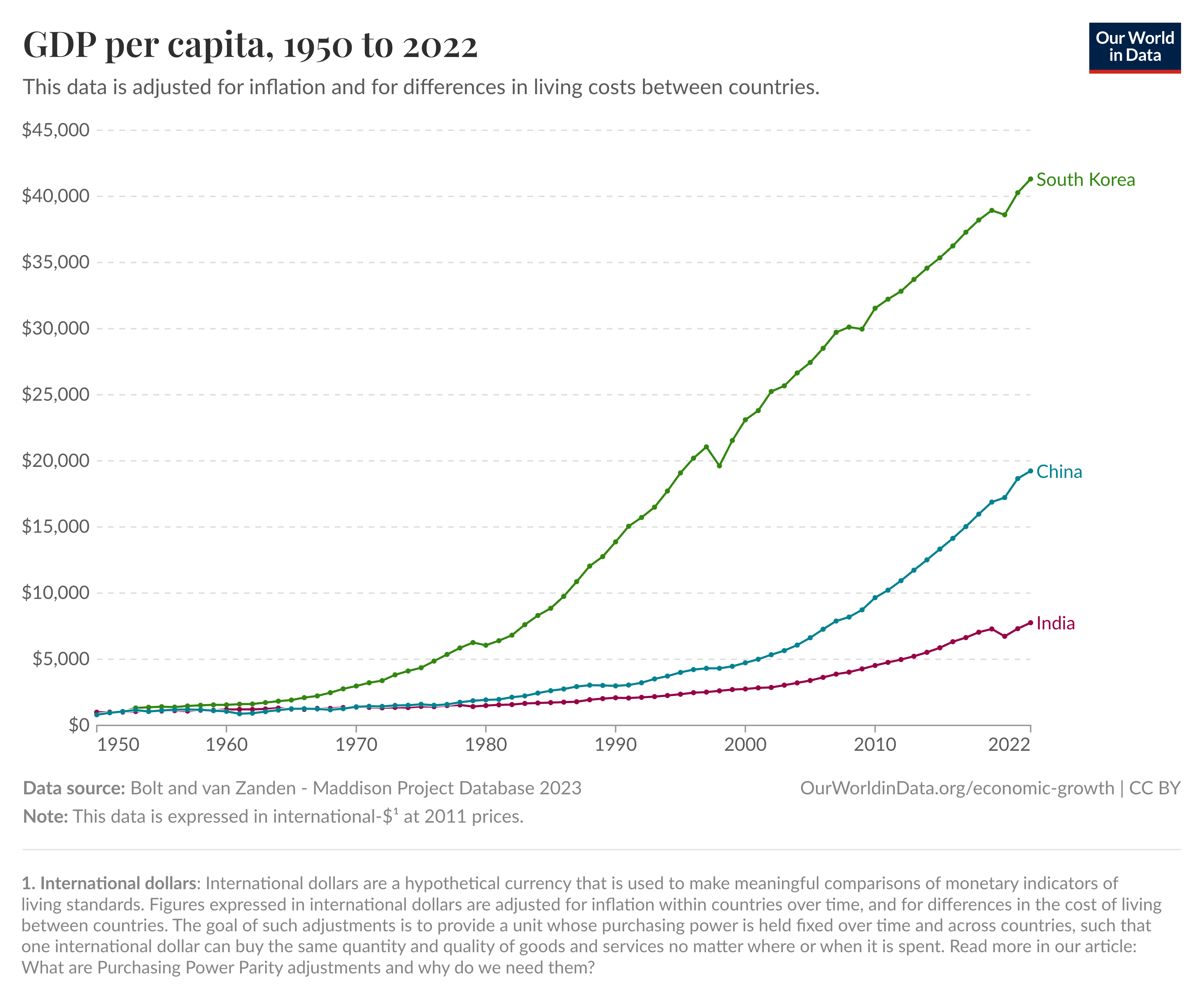

Two countries that have achieved rapid economic expansion over the last fifty years—South Korea and China—offer valuable lessons. They had two things in common: a clear strategy and a focus on export-led growth.

Until about 1980, China and India had roughly the same GDP per capita. Then Deng Xiaoping, the Chinese premier at the time, reformed the economy with his “four modernisations,” which doubled per capita income within 15 years. One of the key pillars of these reforms was a focus on exports—China’s share of world exports increased from around 1% in 1980 to 15% in 2023.

Today, while China faces challenges such as a slowing economy, an ageing population, and a crisis-ridden real estate sector, it is working toward its next phase of growth by moving up the value chain. China is now not only manufacturing goods, but also designing advanced technologies like electric vehicles and making critical breakthroughs in artificial intelligence.

Similarly, South Korea’s per capita income, which was comparable to India’s at the end of the Korean War, is now more than five times higher. South Korea transformed itself into an industrial powerhouse through early economic reforms and a Chaebol, or national champions strategy.

President Park Chung Hee provided subsidies, tax incentives, preferential loans, and domestic protection to corporations—provided these companies met export performance targets. This strategy gave rise to some of today’s largest conglomerates, such as Samsung, Hyundai, and LG, who are global leaders in several industries.

In contrast, India appears to be following a national champions policy without the crucial discipline of tying benefits to export performance. Certain large conglomerates—most notably Adani, Ambani, and, to some extent, the Tatas—receive favourable deals and protection from competition.

However, it is unclear how productively these incentives are being used. This favouritism has also created a climate of fear among businesses outside this inner circle.

Industrial concentration has increased significantly. According to an analysis by former RBI deputy governor Viral Acharya, the proportion of total assets in India's non-financial sectors held by the "big five" conglomerates—Reliance Group, Adani Group, Tata Group, Aditya Birla Group, and Bharti Airtel—rose from 10% in 1991 to almost 18% by 2021.

India’s political economy, at the moment, resembles more the Russian oligarchic model than the South Korean Chaebol model.

It is clear that a dramatic course correction is needed if the Indian economy is to get back on track. Otherwise, India risks getting old before it gets rich. Former chief economic advisor Arvind Subramanian has argued that India may struggle even to become a middle-income country by 2047.

In other news

It is wedding season in India, and here are two wedding ceremony related stories from Meerut. The first report claims that in addition to DJs, weddings now also feature dances by the mare.

The second story is unfortunately a tragic occurrence during the wedding season in parts of north India. Celebratory firing during weddings can often go out of control and lead to loss of life.