Monopoly Money : What is Price gouging?

Kamala Harris has announced that she will bring in a federal ban against corporate price gouging.

One of the tasks that Kamala Harris, presidential nominee of the Democratic Party in the US, has at hand, of course, is to prove that she can protect cats and dogs from hungry immigrants. But she also needs to be able to convince American voters that she can deliver on the economy, an issue on which there is a great deal of anxiety.

One of the centrepieces of her economic plan is a proposed ban on price gouging. So far, Harris hasn’t provided too many details of how the ban would work, other than the plan will include penalties on companies that exploit crises.

Her campaign has shed some light on what they mean by price gouging, especially in the context of grocery prices. “There’s a big difference between fair pricing in competitive markets, and excessive prices unrelated to the costs of doing business,” the campaign said.

The argument is that even corporations that are not monopolies can sometimes be in a position to set the price of their products much higher than the cost, which, Economics 101 (or 102, I am not sure), will tell you should not be possible. Because, as per mainstream microeconomics, in a competitive market, a firm cannot raise prices without the risk of losing market share to competitors.

So, how have firms been able to bypass the immutable laws of microeconomics?

Enter Isabella Weber, a young economist central to an ongoing global rethink on price controls. Her recent work with Evan Wesner, shows that since the COVID-19 pandemic, shortages have meant that certain firms in competitive markets became temporary monopolies and could, as a result, raise prices without the fear of a loss in market share.

The monopoly status arose because supply shortfall meant that demand far outstripped supply and became, to a degree, inelastic – which means consumers were price insensitive. Supply bottlenecks also meant that other firms in the same market could not increase production, and new firms were unable to enter the market for the same reason.

The overall supply, therefore, became limited.

Firms no longer faced the risk of losing customers so they raised prices by an amount greater than the increase in costs. That is how we got what Webber calls “sellers inflation”, or what has more colourfully been described as “greedflation”, or “profitled” inflation

This is quite different from how conventional mainstream economics explains the origins of inflation, in most cases. The argument there is that inflation happens when aggregate demand for goods and services exceeds the capacity of the economy to produce them. And this, the argument goes, happens primarily because of an increase in money supply, or people having too much cash. The solution, therefore is, to reduce money supply by making money more expensive, i.e. by raising interest rates.

Is there evidence that sellers inflation has happened?

There is. Weber and Wesner show that it wasn’t so much increase in labour costs but increased profit margins of corporations that drove inflation in the last 2–3 years.

Initially, they were quite lonely in their analysis and faced a great deal of ridicule and abuse from mainstream economists who found themselves very triggered by the analysis.

But since then, more and more evidence has emerged from around the world including from institutions like the International Monetary Fund (IMF) and the US Federal Reserve, not exactly known for their revolutionary fervour.

Research by the IMF found that corporate profits accounted for almost half of the increase in inflation between 2021 and 2023. It added, “companies increased prices by more than spiking costs of imported energy.”

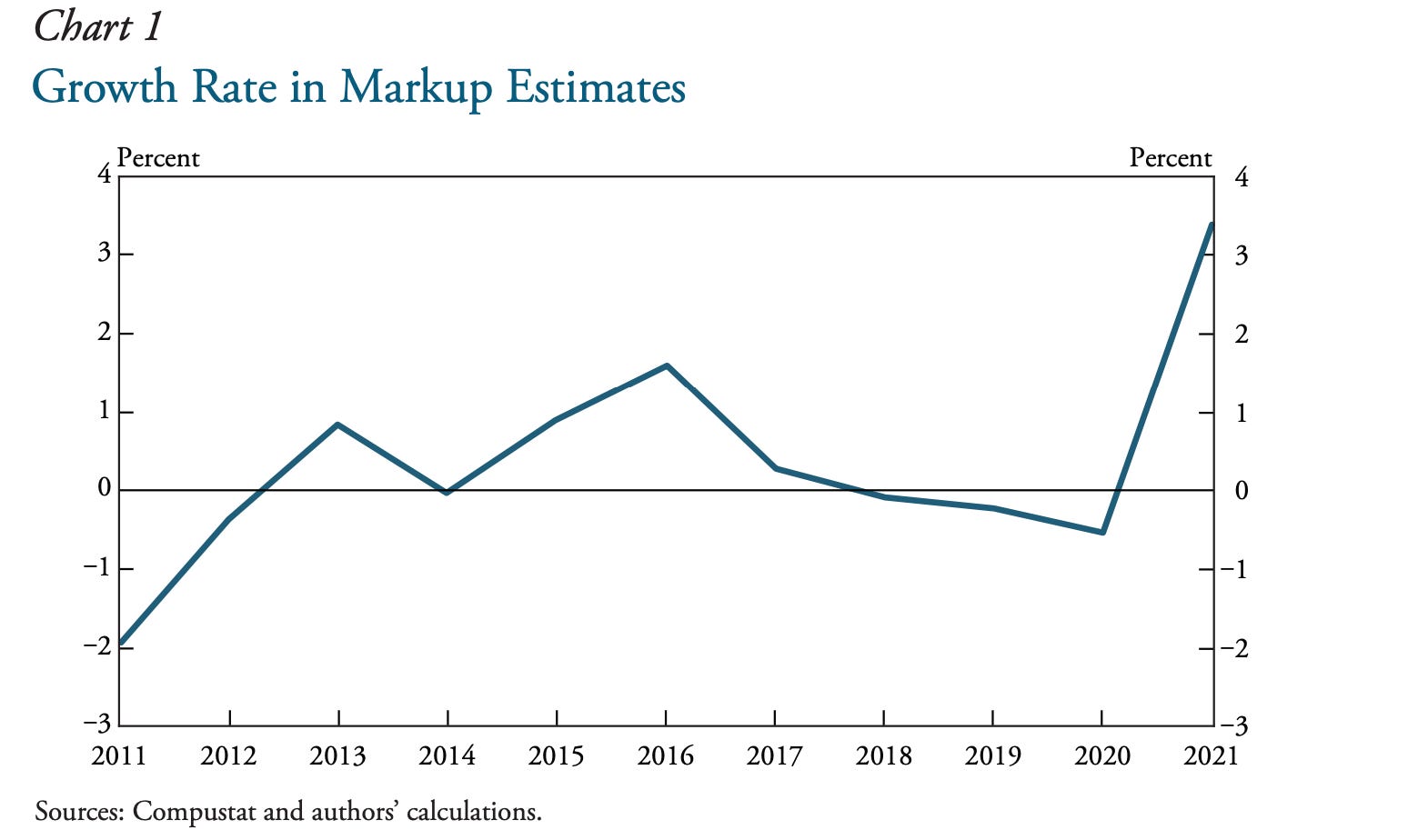

The Federal Reserve Bank of Kansas City found that increased markups accounted for more than half of the 2021 inflation in the US. The contribution was much higher than in the previous decade, as their chart below shows.

Meanwhile, Australia's Competition and Consumer Commission uncovered a different flavour of corporate mischief. They found that two of the country’s biggest supermarket chains, Woolworth and Coles, had misled customers by deceptive discount prices.

The supermarkets would raise the price of products just before placing them on discounts. The ACCC gives the example of the Oreo family pack. Woolworths prices the pack at $3.50 for over 2 years. Then, in November 2022 – around the time when the world was worried about runaway inflation and central banks around the world started increasing interest rates – the supermarket increased the price to $5.

22 days later, the Oreo family pack’s price was dropped to $4.5, and it was placed in the “Prices dropped promotion”, even though the price was about 30% higher than just a month ago.

“Price over volume” is the new corporate strategy.

What are the implications?

Adam Smith, the father of modern economics and founder of the classical free market theory, had observed that profits increase prices exponentially, while wages increase them linearly.

Gita Gopinath, the deputy managing director of the IMF, said in a speech in 2023, that if inflation is to fall quickly “firms must allow their profit margins—which have shot up during the past two years—to decline and absorb some of the expected rise in labour costs.”

But, you can't just force a firm to reduce profit margins. To think of solutions, one must go back to why firms have been able to increase their profit margins? Because of increased monopoly power.

Increasing competition in the market then must be the answer. That is, of course, easier said than done as we live in an age when companies and billionaires have more power than governments.

Proposals to break up these large corporations have been on the table for a long, long time. But, now we are seeing some slow movement on that front. For example, the US government’s attempt to break up Google.

Another measure is price caps. This is essentially what Kamala Harris is proposing to do for groceries. Europe brought in energy and, in some cases, rent price caps after COVID and the Russian invasion of Ukraine.

Taxes on windfall corporate gains have also been part of the discussion. Spain instituted them for energy companies and banks, bringing in $3.2 billion.

Spain also capped energy prices, lowered the cost of public transport and put in quasi rent caps. Over the last two years, inflation in Spain has been lower than elsewhere in Europe.

But, what does one do with interest rates? If inflation is partly an outcome of higher profits, and not because people have too much to spend, then there must also be a rethink on whether raising interest rates is the most effective strategy to contain inflation.

Increasing interest rates is a very painful way of reducing inflation. Its objective is to increase unemployment (which also gives corporations another lever of power over their employees, and they can, for example, ask them to come in to the office five days a week).

Higher interest rates also mean an increased risk of recession because the idea is to slow down the economy. So, central banks attempt to manoeuvre interest rates such that they slow down the economy, but not to the extent that they cause a recession, aka soft landing. And there is no exact science to this, so it’s more a case of aim and hope for the best.

There are no precise answers for the moment, as there perhaps never are in Economics. But, what’s for certain is that the world of Economics is in for a shake up.

Thank you for the great article!